admin

admin

Going to college can be an exciting and rewarding experience, but it also comes with a hefty price tag. In addition to the tuition fees you’ll have to pay, there are other costs associated with attending college that can take a toll on your personal finances and credit score if you’re not careful.

For example, the cost of textbooks alone is enough to make any student cringe. According to the College Board, the average student spends around $1,200 on textbooks and supplies each year.

That doesn’t include miscellaneous items like meals, transportation or housing either. All this extra spending can quickly add up and put a strain on your budget. It’s important to plan ahead and prepare yourself for these additional costs before enrolling in a college or university.

In this article, we are going to cover the associated costs and long-term affects of attending college, using college loans, and how you deal with such debt or those who might co-sign off your further education financials.

The Long-Term Costs Associated with College in 2023 and Beyond

While most people are looking at the immediate out of pocket costs of college, it’s actually the long-term costs associated with college can be even more daunting.

Taking out student loans is a common way to cover tuition fees, especially for those who are unable to pay the entire amount upfront. The problem with this is that loan repayment often begins shortly after graduation, which can lead to serious financial hardship if you’re not careful. Not only will your credit score take a hit due to missed payments, but you’ll also have to start paying interest on the money borrowed.

College is a major investment, and it can have both immediate and longterm costs that can affect your personal finance and credit score.

FAQ on the Major Costs and Investments Associated with College

Here are the answers to some common questions about how college can impact your finances:

Q: How does college affect credit score?

A: Taking out student loans or opening a line of credit for tuition payments may result in an increased credit utilization rate, which could lower your overall credit score.

Also, if you fail to make loan payments on time, this too could adversely impact your credit rating.

That said, successfully completing an educational program can actually benefit your credit history by showing lenders that you are a responsible borrower. In addition, having a degree typically increases earning potential which helps improve debt-to-income ratios and credit scores.

Q: Does cosigning a student loan affect my credit?

A: Absolutely. When you cosign a loan, you become equally responsible for the repayment of that debt and any failure to make payments or defaulting on the loan will have an impact your credit score.

This is why it’s important to understand all of the risks associated with credit implications when cosigning a student loan before taking on this responsibility.

Q: Can college debt ruin your credit?

A: In short, yes. If you are unable to keep up with loan payments or fail to pay them altogether, this could lead to defaulting on the loans and having the debts sent to collections agencies.

This can have a significant negative impact on credit score as well as potential eligibility for future loans. It is important that you understand your loan obligations before taking out any debt and develop a repayment strategy that works within your budget.

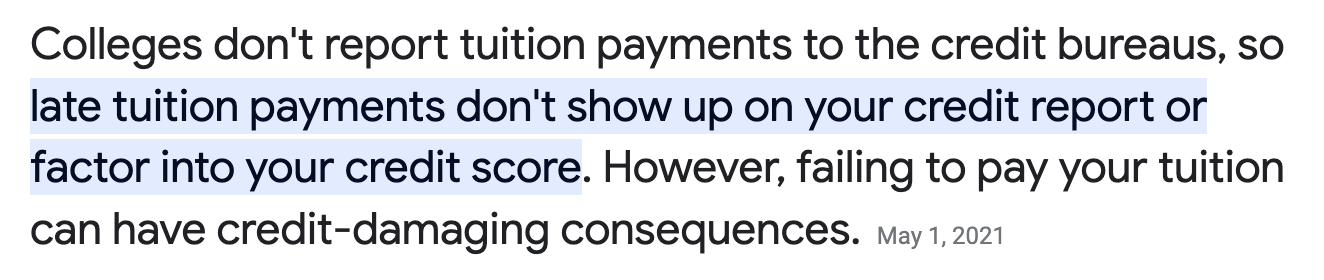

Q: Does paying tuition help build credit?

A: Tuition payments by themselves will not generally improve your credit score since they are typically one-time transactions rather than recurring ones (like loan payments).

However, if you make tuition payments with a credit card and are able to pay off the balance each month, this can help increase your available credit limit which could improve your credit utilization rate.

Additionally, if you use an installment loan (like a personal loan) for college expenses and make regular monthly payments, this can help demonstrate financial responsibility and potentially raise your credit score.

The Real Costs Associated with College and Further Education

At the end of the day, college is not only an investment in knowledge but also in your future financial health. Understanding how the immediate and longterm costs of college will affect your personal finance and credit score is key to making informed decisions on financing options.

With some careful planning and budgeting, you can successfully navigate the world of post-secondary education and get the most out of your investment.

That’s why it’s so important to consider all of the costs associated with attending college before deciding whether or not it’s right for you. Remain mindful of both immediate and long-term costs and don’t overextend yourself when it comes to financing your education. The money you save now could mean the difference between a bright future and financial disaster down the line.

Is College Right for You? That’s for you to decide…

Ultimately, attending college is an important step for many students looking to pursue higher education, but it’s important to be mindful of all associated costs and how they can affect your personal finances and credit score.

By understanding the immediate and long-term expenses involved in pursuing a degree, you can make sure that you’re making the best decision for yourself financially and academically.